According to data from the U.S Census bureau, there are approximately 76.4 million baby boomers living in the United States today. Contrary to what many think, there are very different segments within this generation, and one piece that sets them apart are their housing needs.

John McManus, editorial director of Hanley Wood’s Residential Group says his company “is focusing on the preferences of the younger half, or second-wave baby boomers, as they exhibit different needs than the older boomers.”

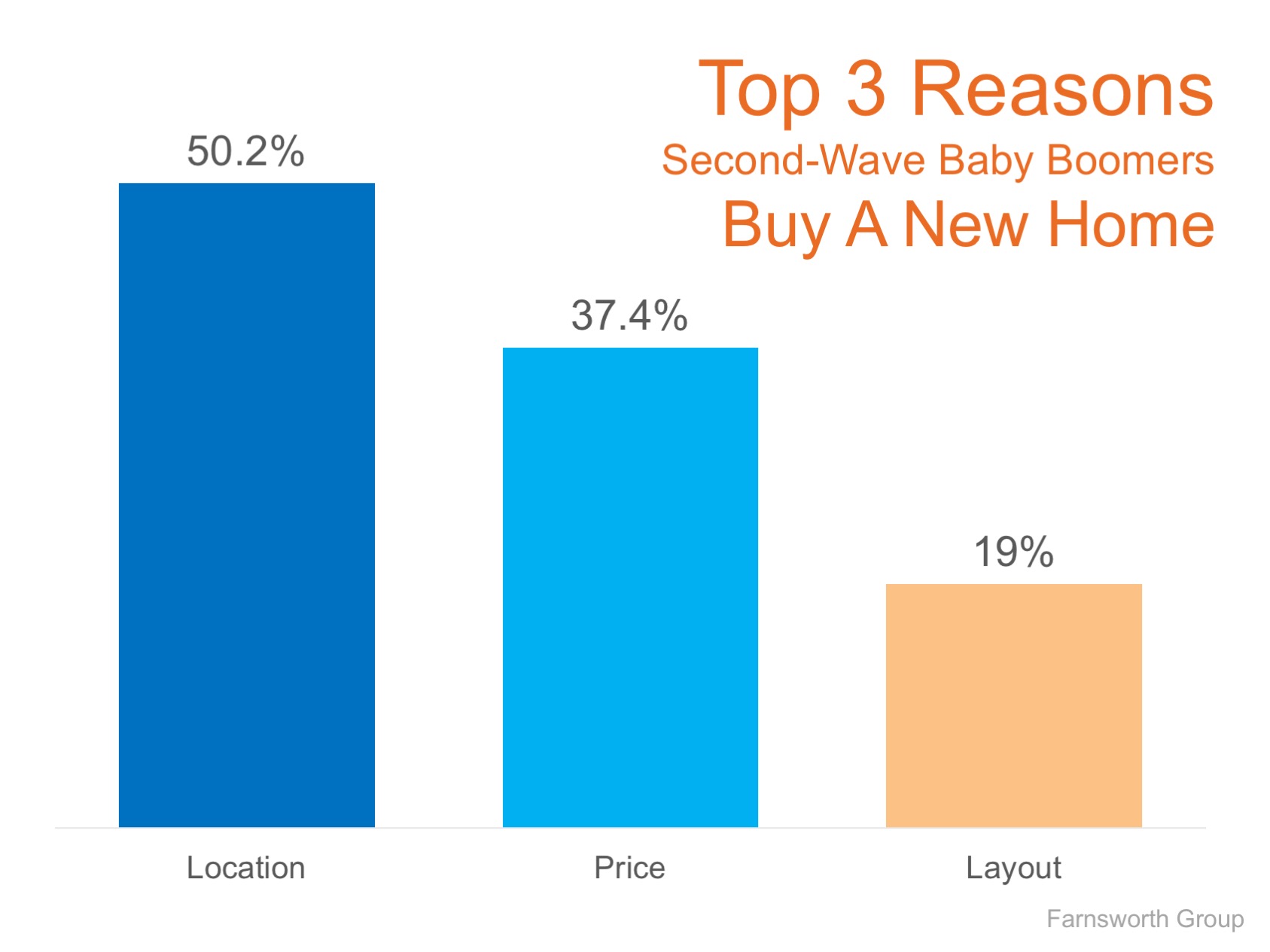

What are ‘second-wave baby boomers’ looking for?

McManus says, “They are seeking a fun, dynamic lifestyle with a home that can also adjust to their changing needs in the future. Living space should either include accessibility features, such as doorway space, lower shelves, and nonslip surfaces, or be easily adjustable when the time comes.”

In a homebuyer study performed by The Farnsworth Group, the participants revealed their reasons for purchasing a new home. The top three factors that influence their purchase include area/location (50.2%), price/affordability (37.4%), and the layout of the home (19%) (as shown in the graph below).

The report also found that when buying a new home, there were other concerns like quality of construction (9%), a safer neighborhood (8.4%), better floor plans (8.25%). The most important rooms or areas are the kitchen (82.8%), master bedroom (59.2%), and great room (36%).

Technology also plays an important role! Second-wave baby boomers prefer wireless security systems (7.1%), lighting that senses and adapts to them (6.3%) and integrated home technology, including “smart” thermostats and lighting controlled by a smartphone (6.2%).

Grey Matter Research and Consulting points to a sense of community as a major factor in wanting to purchase:

“The first impressions are important when entering a new community, as is feeling welcome in the community. Amenities such as clubhouses, pools, and walking trails featured prominently in the decision to purchase in a community. Location was key, as residents want their new homes to be near shopping, dining, medical services and entertainment.”

Bottom Line

If you are one of the many ‘second-wave’ baby boomers who is starting to feel like their current homes no longer fit their needs, take advantage of the low inventory of existing homes in today’s market by selling your current home and moving on to one that truly fits your new lifestyle.

One of the most powerful features of the Home Equity Conversion Mortgage is that the unused portion of the Line of Credit has a built in guaranteed growth factor. So that once the line is established, it will continue to grow regardless of the home’s value. Some have “asked how is this possible?” And the answer is really pretty simple; it was designed into the program in 1988 and has never changed.

One of the most powerful features of the Home Equity Conversion Mortgage is that the unused portion of the Line of Credit has a built in guaranteed growth factor. So that once the line is established, it will continue to grow regardless of the home’s value. Some have “asked how is this possible?” And the answer is really pretty simple; it was designed into the program in 1988 and has never changed.