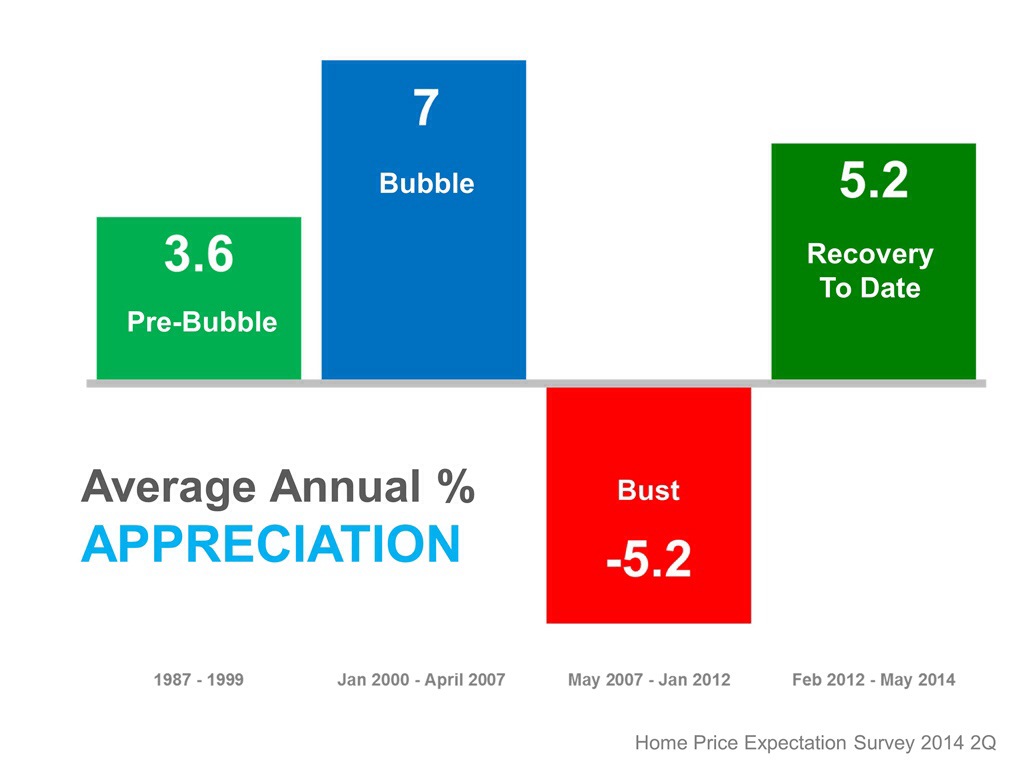

According to the Beracha, Hardin & Johnson Buy vs. Rent (BH&J) Index, the U.S. housing market has continued to move deeper into buy territory, supporting the belief that housing markets across the country remain a sound investment.

The BH&J Index is a quarterly report that attempts to answer the question:

In today’s housing market, is it better to rent or buy a home?

The index examines the entire US housing market and then isolates 23 major cities for comparison. The researchers “measure the relationship between purchasing property and building wealth through a buildup in equity versus renting a comparable property and investing in a portfolio of stocks and bonds.”

While most of the metropolitan markets examined moved further into buy territory (15 of the 23), markets like Dallas, Denver, and Houston are currently deep into rent territory. In these three markets, it is estimated that renting will top homeownership 7 out of 10 times.

Due to a lack of inventory, the home prices in the Dallas, Denver, and Houston, areas have increased by 13%, 11.4%, and 7.3% respectively. Home prices in these areas will begin to return to more normal levels once residents realize that renting is not the best option, therefore bringing home affordability back as well.

Bottom Line

The majority of the country is strongly in buy territory. Buying a home makes sense socially and financially, as rents are predicted to increase substantially in the next year. Protect yourself from rising rents by locking in your housing cost with a mortgage payment now.

To Find Out More About the Study: The BH&J Index and other FAU real estate activities are sponsored by Investments Limited of Boca Raton. The BH&J Index is published quarterly and is available online at http://business.fau.edu/buyvsrent.

![Spring Forward: The Difference An Hour Makes [INFOGRAPHIC] | Simplifying The Market](https://d2d6tznlfad433.cloudfront.net/wp-content/uploads/2017/03/The-Difference-a-Hour-Makes-STM.jpg)