The biggest challenge to today’s housing market is the shortage of housing inventory for sale. A normal market would see a six-month supply of homes for sale. Currently, that number is below four months. This is the major reason home prices have continued to appreciate at higher levels than historic averages.

The good news is that builders are now starting to build more homes in lower price ranges.

Builder Confidence is Up

The Housing Market Index from the National Association of Home Builders (NAHB) reveals that builder confidence increased last month. HousingWire quoted NAHB Chief Economist Robert Dietz about the reason for the increase in confidence amongst builders.

“The HMI measure of future sales conditions reached its highest level since June 2005, a sign of growing consumer confidence in the new home market. Especially as existing home inventory remains tight, we can expect increased demand for new construction moving forward.”

Builders are Meeting the Needs of Today’s Purchaser

Builders are not only jumping into the market – they are doing a better job of matching current demand. The Wall Street Journal recently reported:

“In a shift, new households are overwhelmingly choosing to buy rather than rent. Some 854,000 new-owner households were formed during the first three months of the year, more than double the 365,000 new-renter households formed during the period, according to Census Bureau data.”

The WSJ article went on to say:

“Home builders are beginning to shift their focus away from luxury homes and toward homes at lower price points to cater to this burgeoning millennial clientele.”

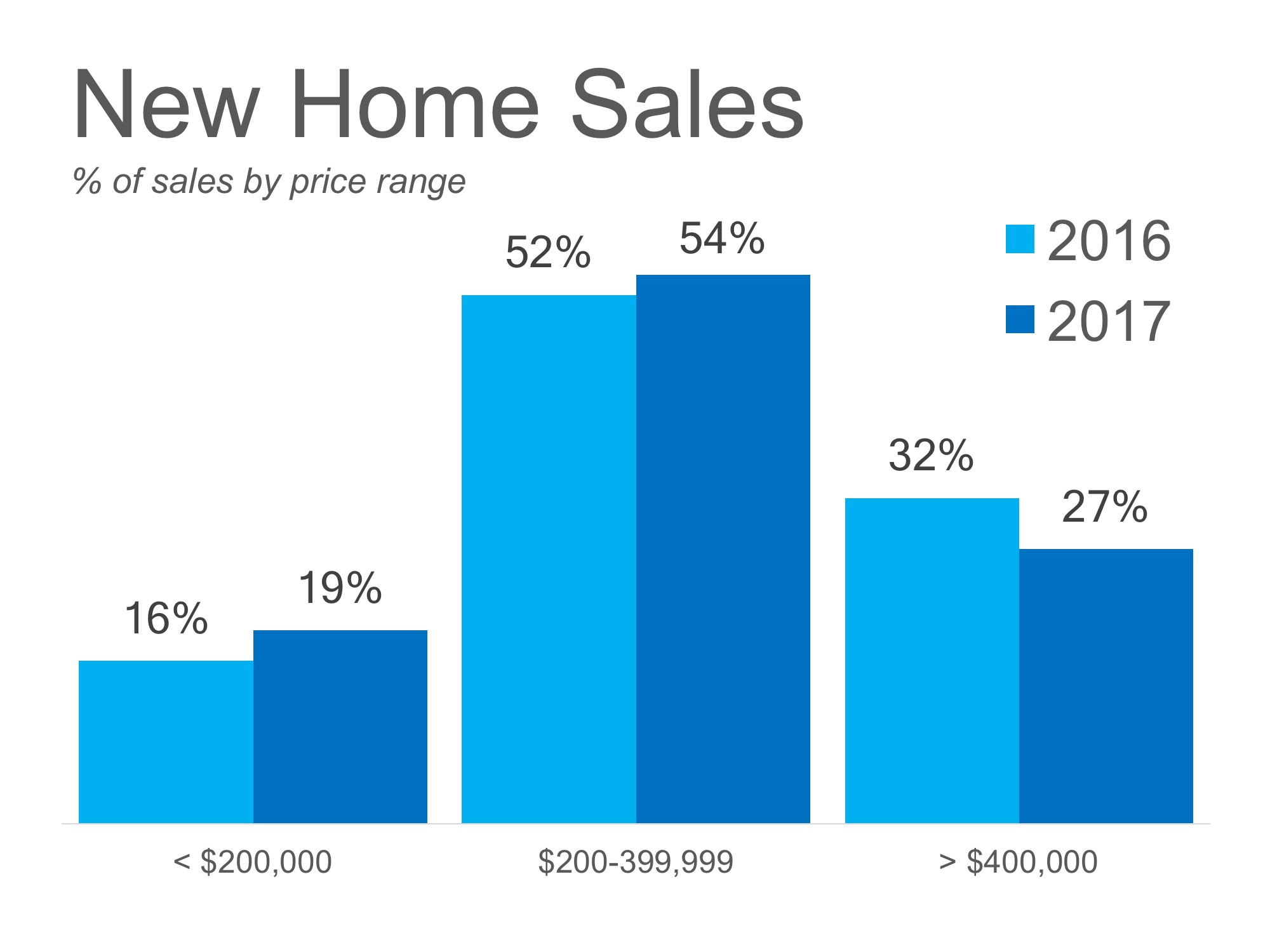

The graph below compares 2016 to 2017 new construction sales by price point. As we can see, builders are slowly beginning to shift to prices more favorable to the first-time and non-luxury buyer.

Bottom Line

There is a drastic need for a larger supply of home inventory to meet the skyrocketing demand. Builders are finally doing their part to help rectify this situation.

![Is Your First Home Within Your Grasp? [INFOGRAPHIC] | MyKCM](https://d8yi0qr1xsq5x.cloudfront.net/2017/04/11134052/FTHB-Demographics-STM-1046x1477.jpg)