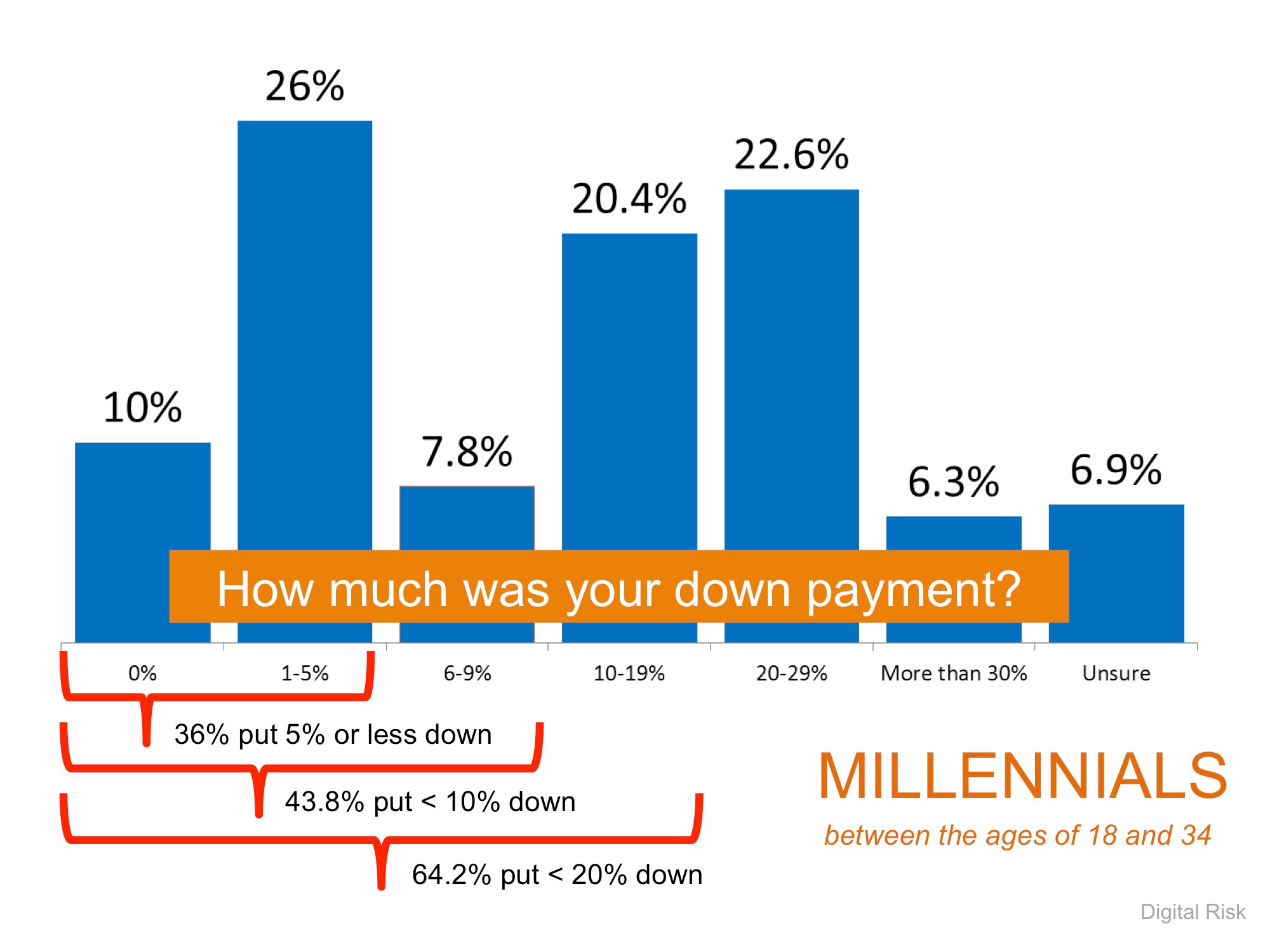

This time of year, many people eagerly check their mailboxes looking for their tax return check from the IRS. But, what do most people plan to do with the money? GO Banking Rates recently surveyed Americans and asked the question – “What do you plan on doing with your tax refund?”

The results of the survey were interesting. Here is what they plan to do with their money:

- 41% – Put it into savings

- 38% – Pay off debt

- 11% – Go on a vacation

- 5% – Make a major purchase (car, home, etc.)

- 5% – Splurge on a purchase

Upon seeing the research, The National Association of Realtors (NAR) wondered if this could help with a constant challenge cited by many people who wish to purchase a home – saving for the down payment.

In a recent post in NAR’s Economists’ Outlook Blog, they explained:

“With a sizable tax refund, the average American would have a decent down payment depending on which region or market you live in.”

They went on to add:

“Approximately 5 percent of all respondents indicated they would make a major purchase which does not seem like a lot. However, there is a bigger group 41 percent who see saving the tax return is best and that group could be potential homebuyers if they are not already.”

In other words, putting that money toward purchasing a home is a form of savings.

Bottom Line

When one considers that first-time home buyers in 2016 had an average down payment of 6%, a decent tax return could go a long way toward the necessary funds needed for a down payment on a house. Or perhaps, the down payment needed by a son or daughter to make their homeownership dream a reality. How are you going to spend your return?